FIFO (First In, First Out) sells the oldest inventory first; LIFO (Last In, First Out) sells the newest inventory first. The choice affects your cost of goods sold, your reported profit, and your tax bill — especially when prices are changing. Most businesses use FIFO; LIFO is only allowed in some jurisdictions (US permits it; IFRS does not).

FIFO vs LIFO at a glance

Most FIFO vs LIFO guides stop at the definitions. The interesting question is which one fits your business — and that depends on what you sell, where you report, and how fast your input costs are moving. The same comparison is searched both ways — FIFO vs LIFO and LIFO vs FIFO — because the two methods are mirror images of each other. Here's the whole decision in one table.

The headline: FIFO is the global default. It's allowed under every major accounting standard, it matches how inventory physically moves in most businesses, and it produces financial statements lenders and investors can actually read. LIFO isn't really an "accounting method" in the everyday sense — it's a US-only tax strategy that happens to be implemented through inventory accounting. If you're not deliberately pursuing that tax strategy with a CPA, you're using FIFO.

What is FIFO?

FIFO — First In, First Out — is the inventory method where the oldest units you bought are the first ones charged to cost of goods sold when you make a sale. The name describes both the accounting treatment and the physical reality on the warehouse floor.

Think about the milk in a grocery store. New cartons go at the back of the shelf. Shoppers pull from the front. The oldest stock sells first. That's FIFO — not a tax-engineering trick, just common sense for anything that can expire, degrade, or go out of style. If you sell physical products and you're not deliberately doing something clever for tax reasons, this is almost certainly how your inventory already moves.

FIFO is the accounting default for three reasons. It matches the natural flow of stock for the vast majority of businesses — bakeries, pharma distributors, e-commerce 3PLs, anyone tracking batches with dates. It's the only method permitted under IFRS, the standard used in over 140 countries — so if you ever want international investors, an overseas listing, or a non-US acquirer, FIFO is your only option. And it leaves your balance sheet inventory valued at recent purchase prices, which lenders and investors can interpret without a footnote.

The one meaningful trade-off: when input prices are rising, FIFO produces higher taxable income — because the older, cheaper costs flow through COGS while revenue reflects today's prices. In our worked example below, that gap is $400 of extra reported profit and about $100 of extra tax. For most businesses, simplicity, global applicability, and clean financial statements are worth the difference. For a US business sitting on millions of dollars of slow-moving inventory in a high-inflation industry, the math can flip — which is exactly where LIFO comes in.

What is LIFO?

LIFO — Last In, First Out — is the inventory method where the most recently purchased units are the first ones charged to COGS when you make a sale. It's the opposite of how inventory physically moves in almost any warehouse — and that's the point. LIFO isn't a description of how stock flows; it's a tax strategy that's been wedged into the inventory accounting framework.

It caught on with US retailers and manufacturers in the 1970s, when double-digit inflation made the math irresistible. The logic is simple: when prices are rising, your newest stock always costs more than your oldest. Match the newest (higher) cost against today's revenue first, and you report a lower gross profit. Lower profit means a lower tax bill this year. The cash you don't send to the IRS stays in your business as working capital. For a steel distributor with $20M of slow-moving inventory in a 4% inflation year, that can be a six-figure deferral, every year.

The catch is the LIFO reserve — the cumulative gap between what your inventory is worth on the books under LIFO and what it would be worth under FIFO. As prices rise, the reserve grows, and your balance sheet inventory drifts further from any number connected to reality. This is why bankers underwriting a line of credit will often add the LIFO reserve back to inventory before they trust the figure, and why a business looking strong operationally can look smaller on paper.

The hard constraint: LIFO is prohibited under IFRS. If you're based outside the US, or you might raise from international investors, or you could be acquired by a non-US buyer, LIFO simply isn't on the menu. Even within the US, electing LIFO is a one-way door — switching back triggers a taxable event that can wipe out years of deferred savings in a single year, plus IRS Form 3115 paperwork. You don't try LIFO; you commit to it.

Worked example (same numbers, two methods)

Here's the cleanest way to see the difference. You're a wholesaler. You bought stock in three monthly batches at steadily rising prices, and in March a customer order takes out 150 of those units. Same purchase history, same sale — but FIFO and LIFO send you to your accountant with very different numbers.

FIFO reports $1,400 gross profit; LIFO reports $1,000 gross profit — a difference of $400. At a 25% tax rate, LIFO saves $100 in current taxes. The trade-off: LIFO leaves a lower, older inventory valuation on your balance sheet — the so-called “LIFO reserve.”

Take a second with that $400 gap. Nothing physical changed — the same 150 units left the warehouse, the same $3,000 hit the bank, the same 150 units sat on the shelf at month-end. The only difference is which cost layer the accountant matched against the sale. FIFO drew from the $10 January batch first; LIFO drew from the $14 March batch. That single decision moved gross profit by $400 and your federal tax bill by roughly $100 at a 25% rate. Multiply that by every quarter, every SKU, for a decade of rising prices and you start to see why LIFO elections are sticky.

Which should you use?

Honest answer: if you're reading this to figure out which one to pick, you almost certainly want FIFO. The LIFO vs FIFO decision is rarely a coin flip — LIFO is the right choice for a narrow slice of US businesses with a specific profile, and if you fit that profile, you already have a CPA telling you so. Here's the test, in two cards.

Use FIFO if…

- You sell perishable goods (food, pharma, cosmetics)

- You report under IFRS or might in the future

- You want financial statements investors trust

- You operate outside the United States

- You want inventory values to reflect current market cost

- You are building or growing a business to sell

Use LIFO if…

- You are US-based and report under US GAAP only

- Input prices are consistently rising

- Tax deferral is an explicit short-term priority

- You have large, stable inventory (e.g. bulk commodities)

- You have a CPA advising specifically on LIFO elections

- You do not plan to report internationally

If you're genuinely weighing a LIFO election, do not do it on the strength of a blog post — yours included. The election goes on your tax return for the year you adopt it, it locks in for your financial statements too, and unwinding it can cost more in one year than it saved you in ten. A CPA needs to model the deferral against three things: the LIFO reserve you'll accumulate, what happens if your inventory levels ever drop (LIFO liquidation), and the restatement cost if you ever need IFRS-compliant numbers for an investor or acquirer. For most growing businesses, the LIFO vs FIFO answer comes out the same: FIFO, and put the energy you'd have spent on LIFO compliance into inventory management that reduces waste.

Other inventory methods

FIFO and LIFO are the two most widely discussed, but they are not the only options. Three others are worth knowing — especially if your inventory has unusual characteristics.

For most product-based businesses, the practical choice is between FIFO and Weighted Average Cost. FIFO wins when batches genuinely differ — expiry dates, lot numbers, quality grades, supplier provenance. Weighted Average is simpler and works fine for truly fungible bulk goods (think gravel, fuel, raw grain) where tracking individual units adds no value. If your suppliers are inconsistent enough that batch tracking matters operationally, see our vendor management guide — bad supplier discipline is what makes FIFO compliance hard in the first place.

How to implement FIFO in your warehouse

Picking FIFO on your tax return is the easy part. Making it true on the warehouse floor — where pickers grab whatever's closest to the door at 4:55pm on a Friday — is where most businesses quietly drift back to "newest first" without realising it. The five practices below are what keeps FIFO honest. None of them are about accounting; all of them are about layout, labels, and discipline.

- 01Label every pallet and shelf with a receive dateThe most important physical habit. When stock arrives, stamp or tag it with the date received before it goes on the shelf. Use a date gun, adhesive labels, or your WMS barcode system. Without visible dates, pickers default to whatever is easiest to reach — usually the newest stock at the front.

- 02Receive new stock to the back, sell from the frontThis is the warehouse rule that makes FIFO automatic. When replenishing shelves, new product goes behind existing stock. Pickers always take from the front — and the front always holds the oldest inventory. Gravity-fed flow racks make this foolproof in high-volume environments.

- 03Create pick paths that follow age, not locationIn a well-organised warehouse, older stock is naturally at the front and newer stock at the back. Your pick lists should direct pickers to the oldest location first. WMS software enforces this automatically — pick locations are suggested in FIFO date order.

- 04Enforce receiving discipline at every inbound shipmentFIFO breaks down when receiving is rushed. Designate a receiving zone, record the date and batch number at intake, and never put mixed-date product in the same bin. Each bin should hold one purchase batch — this makes date management auditable.

- 05Reconcile your inventory system daily or weeklyPhysical FIFO only works if your system reflects reality. Perform regular cycle counts — focus on fast-moving SKUs first. When physical counts diverge from system counts, investigate the cause before it compounds. FIFO errors compound quickly: if you charge the wrong batch cost, your COGS and tax figures are both wrong.

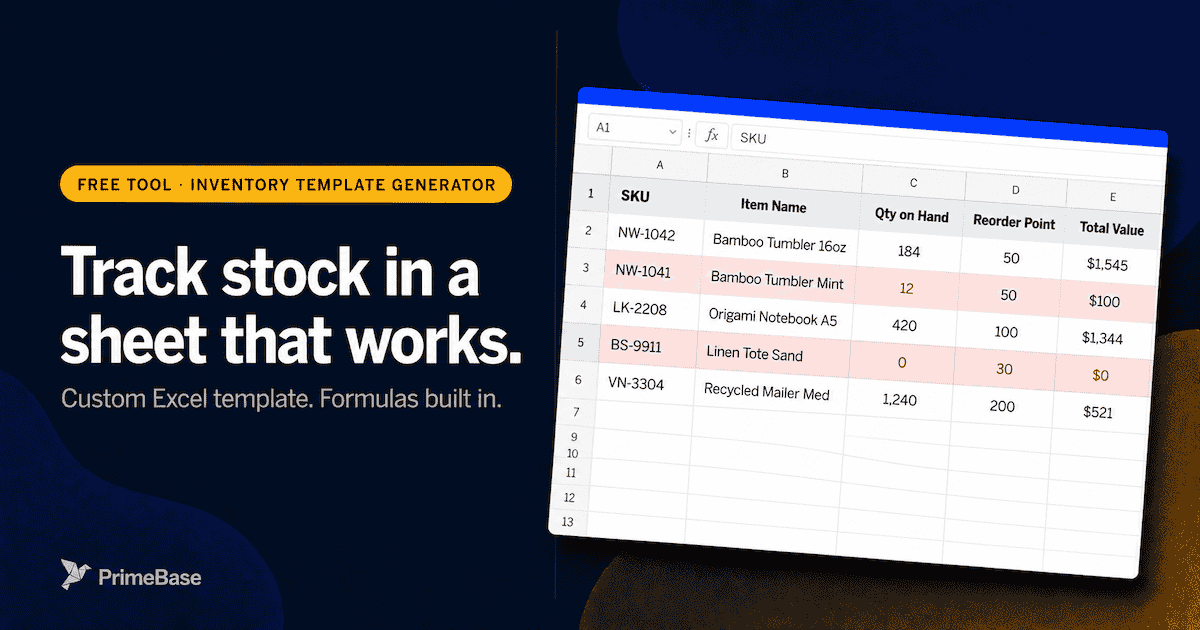

Track inventory in Excel — batch-dated and FIFO-ready.

Multi-sheet template with example rows, data validation, and a batch-date column so FIFO order is visible at a glance. Excel + CSV export.

How PrimeBase handles FIFO and LIFO

PrimeBase supports both FIFO and FEFO picking out of the box — track inventory by batch with expiry dates, and the system enforces the right pick order automatically. Every stock movement automatically posts the correct COGS entry based on your chosen method. No manual reconciliation, no end-of-period catch-up.

See how it works: inventory management · accounting & COGS

Frequently asked questions

Practical guides on SOWs, invoicing, client onboarding, and the tools that save real time — written for people who run service businesses.